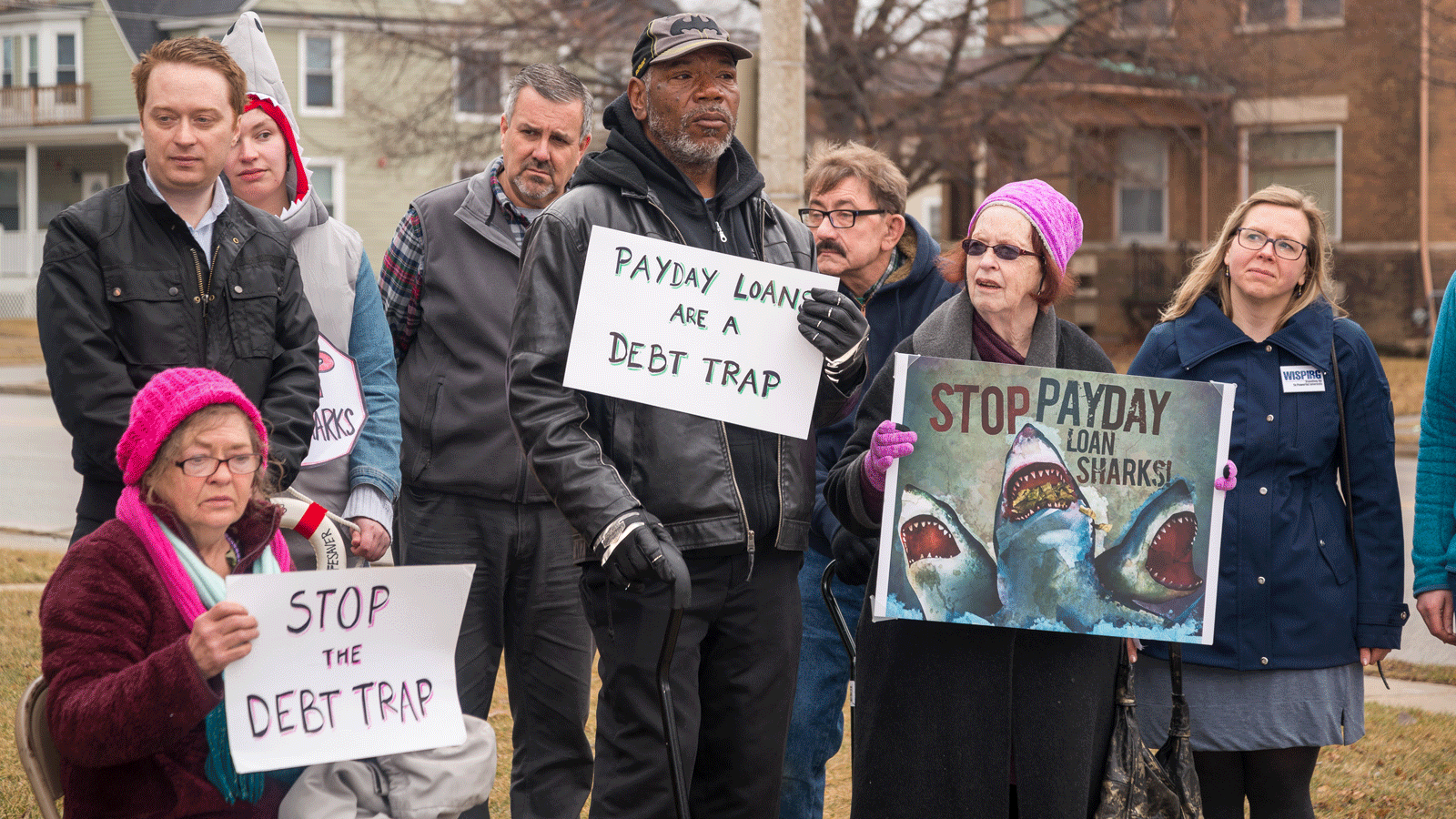

To protect consumers in the financial marketplace, we're working to reform credit bureaus, stop predatory loan sharks, end unfair banking practices and more.

Tell insurance CEOs: Stop insuring climate risks

Senior Director, Federal Consumer Program, PIRG

Director, Consumer Campaign, PIRG